Welcome

Hey there Early Stagers… You probably noticed that I finally decided to listen to the multiple complaints I received from readers and changed the font to one that’s easier to read…

I also removed the news section as it was very tedious for me to compile and I assume it has little value here. Please let me know if this is not the case (simply email me at: avinoam@buildingstartups.net) and I can bring it back in the future.

This week it’s all about Investors and valuations. You are going to learn how to filter down and find the right investors for your startup and understand how investors value it.

So, lets not waste any more time and dive right in…

Yours truly,

Avinoam

How to Choose the Right Investor

There are 2 approaches to fundraising:

- Spray and pray – Send your deck to any one you can and hope something sticks

- Intentional – Choosing the right people you want and going out to get them

Which do you think is best?

On one hand, everybody is saying that it’s a numbers game, that you have to hear a lot of no’s until you get to the one yes. Which indicate that the spray and pray method the right choice.

But this is wrong on so many levels…

Why S&P is wrong

Working in the Spray and Pray method is like going to a bar and asking everyone you meet to go on a date. You might hit one that’s going to say yes, but is that the kind of person you want to be with?

Furthermore, you are in for plenty of ups and down. You want the right people with you to give you the right advice and support. If you bring in the wrong investor in you can find yourself having to battle not only the market, but also your board. And that’s someone who can kick you out of your own startup.

The last nail in the coffin is your time and energy. Taking on pointless meetings with irrelevant investors, just because they said yes is a bad idea and a recipe for a lot of frustration for so many reasons.

I think it’s safe to say that you have to be a lot more intentional in the investor vetting process. So, what criteria should you use?

How to Narrow Your List

To narrow your initial investors list you need to know how to filter it. Here are the criteria I recommend you use:

- Stage

Only target investors who invest in your type of round. Earlier rounds have higher risk and not all investors are open to it. Going after an investor that’s not investing in your stage is simply a waste of time. - Industry

Most investors are industry agnostic, which means they only invest in specific industries. The reason for this is the added value they can bring and their ability to gauge the risk associated with investing at that industry. They simply know the industry therefore are more open to taking risk in it. - Geography

Most investors like to be close to their investments (this is changing with the globalization, competition and teleconferencing capabilities like zoom) which means they only invest in specific geographic location. Another reason for this can be the legal and corporate structure and market familiarity. Regardless of the reason, just make sure you approach investors that are open to investing in your geography. - Competition

Most investors don’t have the luxury of making multiple bets in a single race (solving the same problem). This means that if an investor had already made an investment in your direct competitor, odds are that he (or she) will not make another investment in you. So, check for their portfolio before you approach. - Lead/Follow

Every investment round has a lead investor. This is the investor that puts in the lion share of the money and occupy the board seat. The lead investor will also help you bring more investors onboard (usually investors that he or she knows or worked with in the past) and help you close the round. This is why you should start with finding a lead investor first and only then move to add more investors.

But we’re not done yet. Once you have a shorter list of relevant investors, you can shrink the list even further. Here’s how

The Human Factor

The investor you are going to bring in to your company is going to have a lot of influence on how you will operate in the future. This means that it has to be a person you are able to work with. Someone who you can come and consult with in bad times and be open to listen for advice.

To get this information, you should approach portfolio entrepreneurs of each investor on your list and ask them about working with that investor.

Ask about communication style, board ethics, risk tolerance, have they ever fire a CEO, and how are they when things go south. The answers to these questions will give you a great indication on what it will be like on e the day after the investment.

Remember that once an investor give you money, you are giving away a lot of control in your own startup. Bringing in the wrong investor can cut your wings and make your life a living hell. On the flip side, bringing in the right investor can give you a layer of confidence and support that will get you through some rough times.

The above conversations are a great way to get warm intros. It’s exactly the ice breaker you need to start up a relationship with another entrepreneur (which has a lot of value on its own merits) that can later recommend you to your target investor.

Once you have a short list of relevant and potential investors it’s time to roll up your sleeves and get to work. Next week we will cover how to get to investors, so subscribe to the newsletter so you want miss out.

And in the meantime you can start your investors search here

Never miss an update

Subscribe to our newsletter to get the latest updates on everything early-stage related.

How much is my Startup Worth?

That’s the question every founder ask himself at every funding round. Without a way to find that number how can you know how much equity should you give investors for their money.

In mature companies with profits and assets, getting to a valuation is nothing more than an accounting exercise. But when it comes to early-stage startups, which most of the time do not have any revenue, or that are not profitable, getting to a number is a little more complicated.

This is of course not a new problem and there are many methods to solve it. Choosing the right method depends on the startup’s situation, the relevant information available, and of course some bias depending on who is doing the valuation.

We’ve summarized the top 12 methods for early-stage valuation in a guide with detailed instructions on when and how to use which method. You can download the guide by pressing the below button.

LinkedIn Treasure Trove

Every day I go on LinkedIn and every day I find great content that can help early-stage founders. Sure, some of it is very superficial, and some is not require more digging to actually be useful. But there’s no denying it, there’s a lot of knowledge out there.

I gathered some of my favorite pieces so you can expand your mind…

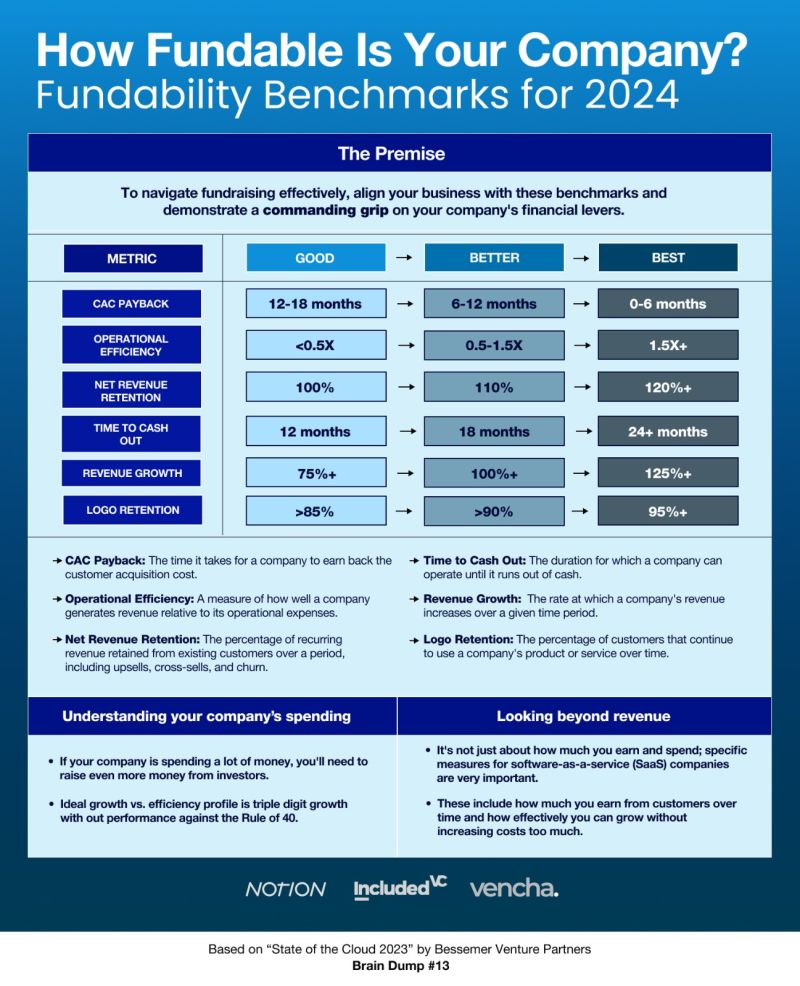

This post gives you some great benchmark to hit if you want to get your startup funded (based on state of the cloud 2023). Link to original post

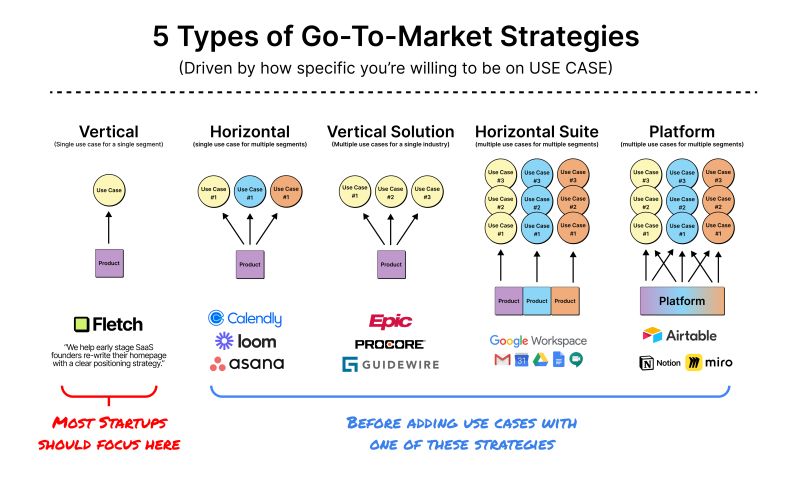

Is having multiple use cases good for your startup? yes and no. It really depend on how well you can manage the complexity of the GTM. Here’s a nice breakdown of companies who did it well

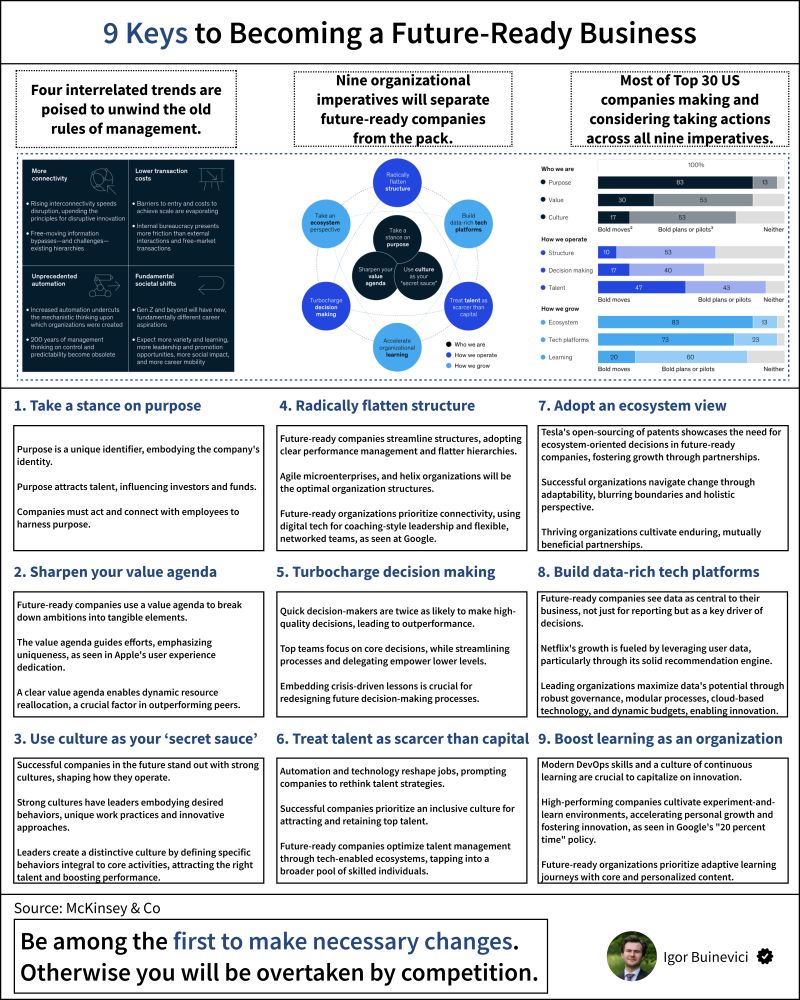

These 9 keys are from McKinsey, but they hold true for startups as well. Read the original post.

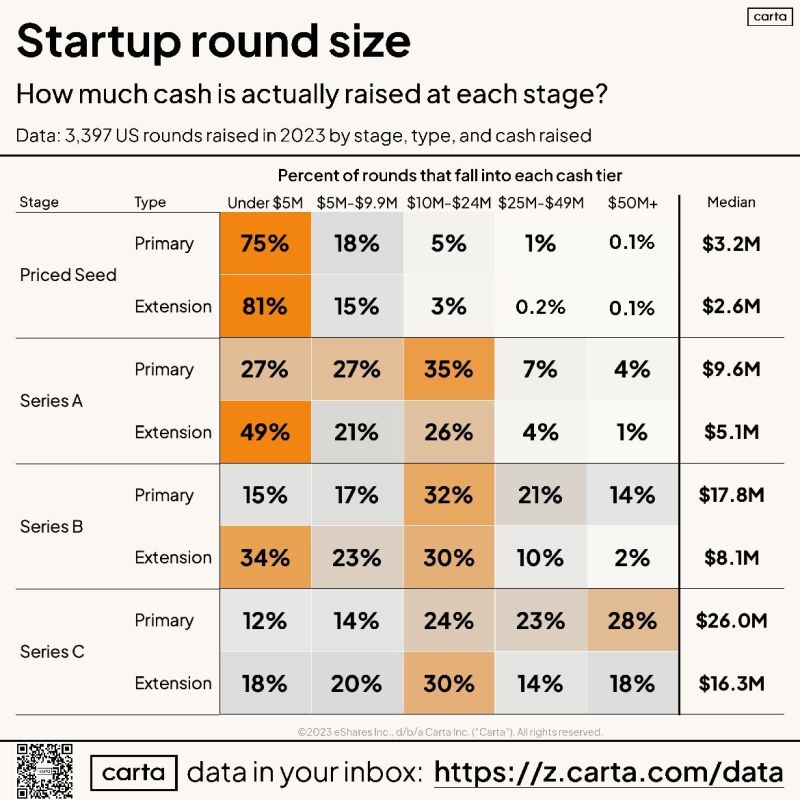

A recent data from Carta showed a large range of valuations for each round. This means that just the valuation, or check size is not a good indicator of round definition. So what is? Milestones… This article explain how

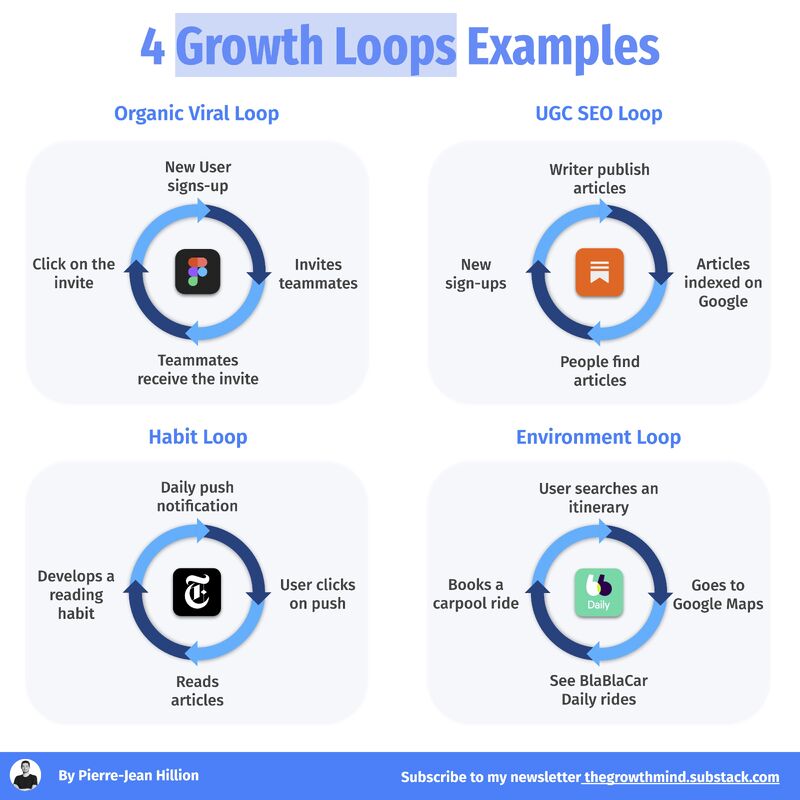

This article has a breakdown of 4 growth loops you can use in your startup. Read it here…

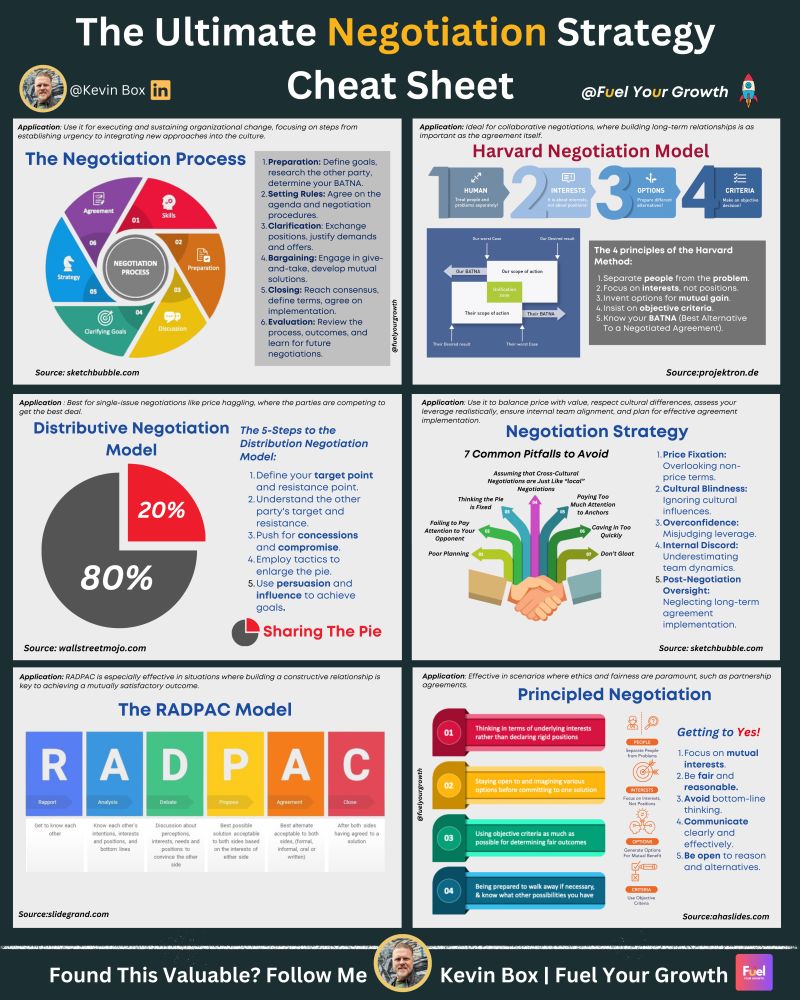

Negotiations are a part of every startups day to day activities. If it’s with investors, customers and even suppliers. To close a deal we all must negotiate. Here’s a cheat sheet to help you improve your negotiation skills.

Here is a great framework to analyze why your marketing does not work and what to do about it.

A great way to launch your cold outreach is by email. It can be personalized, mass mailed and give you an ability to scale. But getting your email to be opened, let alone read is super hard. Here’s a crash course on how to do it.

We’ve already talked about the variations in check sizes per round, but what is the avg. according to the data (from Carta.)

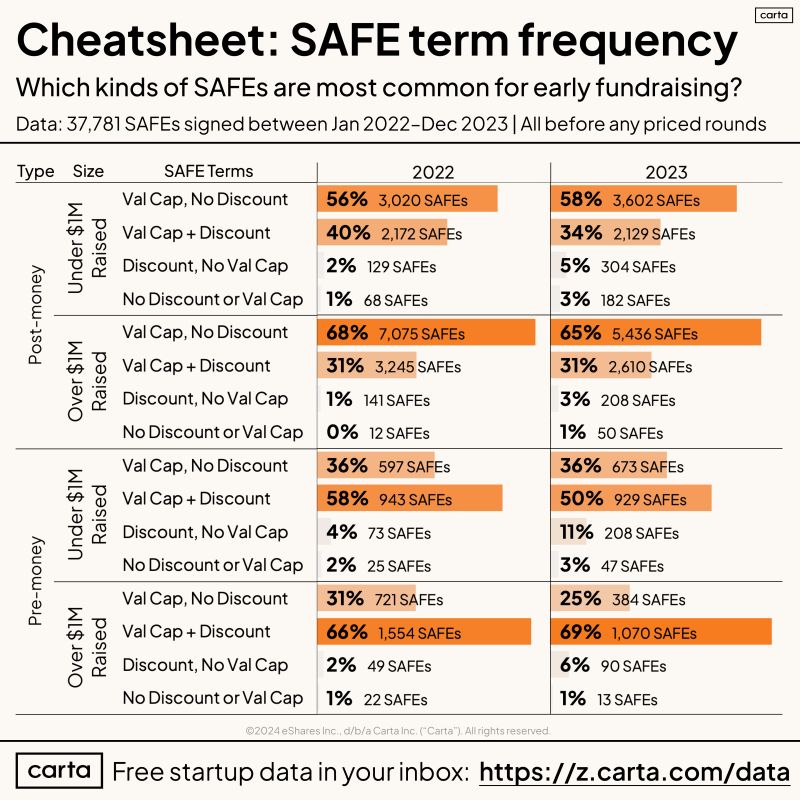

SAFEs are the most common investing vehicle in early-stage funding. But it has some levers you can play with. It’s interesting to learn how different founder structure their SAFEs. Here is the data.

Here are links to 6 FREE courses on leadership from the top universities.

I’ve already stated how common SAFEs are, but do you even know what they contain? Here is a great article that explain it very well.

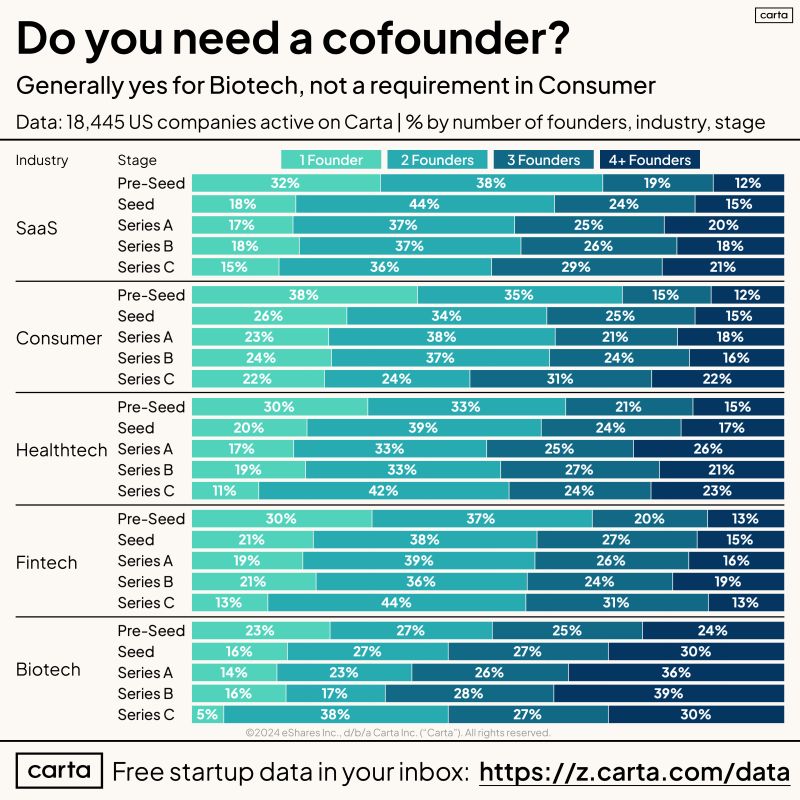

The debate of the best size for a founding team is a long argued debate. Investors have been saying that a solopreneur is unlikely to succeed as a founding team. But are they right? The data doesn’t lie, so get the truth right here.

Never miss an update

Subscribe to our newsletter to get the latest updates on everything early-stage related.